Key Takeaways

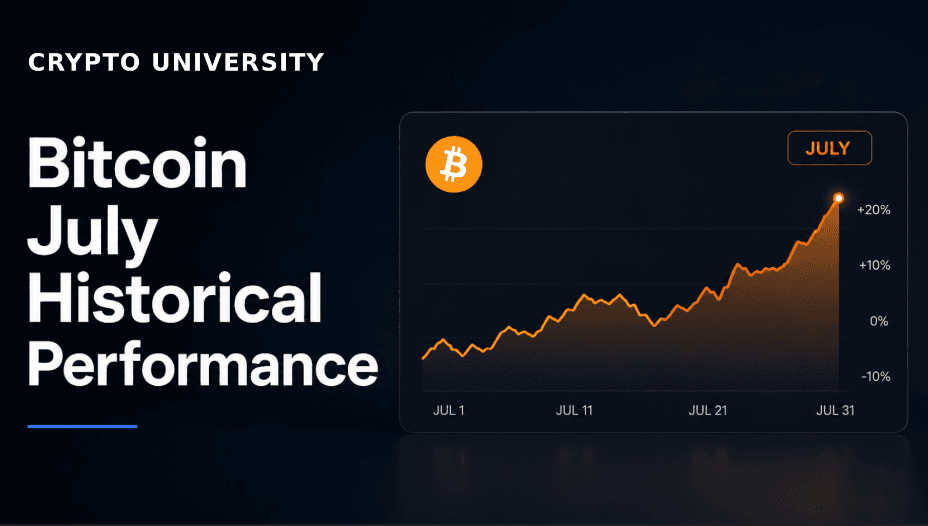

Historical data shows July has delivered positive average returns for Bitcoin in most years since 2013, often cited as one of its stronger months on average.

The “bullish July” narrative typically highlights recovery patterns after weaker June periods, though these observations come from a limited dataset and do not guarantee similar results.

Seasonal narratives provide market context and can influence sentiment, but they represent just one data point among many and should be evaluated alongside broader fundamentals and risk considerations.

What Is the “Bullish July” Narrative for Bitcoin?

In financial markets, seasonal patterns refer to recurring tendencies in asset performance tied to specific times of the year. For Bitcoin, some market observers and analysts point to July as historically one of the stronger months. This has led to discussions of a “bullish July” narrative, especially in periods following weaker June performance or during broader market recoveries.The narrative gained attention in mid-2026 amid conversations about potential seasonal strength. Analysts often reference data showing that June has frequently posted modest or negative average returns, while July has shown a positive bias on average. This contrast sometimes fuels expectations of a “July bounce” or relief rally.It is important to note that these patterns are descriptive of past price movements only. They do not imply causation or future outcomes. Bitcoin’s market has evolved significantly since its early years, with increased institutional participation, regulatory developments, and macroeconomic influences that can override any calendar-based tendencies.

Historical July Performance Data

Reliable trackers and analyses of Bitcoin price data since 2013 provide the following overview of July performance:

Average return: Approximately 7% to 7.6% across multiple sources and datasets.

Median return: Around 8% to 8.9% in several studies.

Win rate: Positive returns occurred in roughly 9 out of 13 years (about 69%) in one detailed review covering 2013 onward.

Variability: Returns have ranged from strong double-digit gains in some years to modest losses or near-flat performance in others.

Selected Historical July Examples (approximate returns from aggregated data sources)

Year | Approximate July Return | Context |

2013 | +8–9% | Early bull market phase |

2014 | Mixed to slightly negative in some datasets | Bear market period |

2015 | +8–11% | Recovery year |

2016 | +11–12% | Pre-halving strength |

2017 | Near flat to modestly positive | Bull market year |

2018 | +9–21% (source variation) | Bear market recovery attempt |

2019 | Mixed, some datasets show modest gains | Sideways to recovery |

2020 | Strong gains (~+24% in peak reports) | Post-crash recovery and bull run |

2021 | Positive mid-single to high teens | Bull market continuation |

2022 | Positive double-digit in several trackers | Bear market but notable bounce |

2023 | Modest negative (~ -3% to -4%) | Post-FTX recovery phase |

2024 | Strong positive (~+14%) | Bull market year |

These figures can vary slightly between data providers due to differences in exact price sources (e.g., daily closes) and calculation methods. The key observation across sources is a positive average with notable year-to-year differences.For comparison, other months show their own historical tendencies. November has often recorded the highest average returns in longer-term datasets, while September has frequently been weaker. Such month-by-month breakdowns help illustrate that no single month dominates consistently every year.

Why Do Analysts Discuss July Strength?

Several factors are commonly mentioned in connection with observed July performance:

Post-June recovery dynamics: June has shown weaker average returns in some multi-year periods. This can create a statistical rebound effect in the following month as selling pressure eases.

Market cycle timing: In certain post-halving cycles, summer months have coincided with phases of accumulation or reduced selling from earlier cycle participants.

Liquidity and participation patterns: Summer periods sometimes feature lower overall trading volumes, which can amplify price moves in either direction once momentum shifts.

Broader sentiment cycles: Media coverage and trader positioning around calendar events can create self-reinforcing short-term flows.

These explanations remain hypotheses. Bitcoin’s price is influenced by a wide range of variables, including global liquidity conditions, regulatory news, technological developments, adoption metrics, and macroeconomic events. Attributing performance primarily to the calendar month overlooks these dominant drivers.

Limitations of Seasonal Narratives

Seasonal analysis in any market, including cryptocurrencies, has important constraints:

Small sample size: Bitcoin has meaningful price history for only about 15–17 July periods with sufficient liquidity and data quality. This is a very small dataset for drawing statistical conclusions.

Changing market structure: Early Bitcoin (2013–2017) operated in a far less mature environment than today’s market with spot ETFs, institutional custody, and global regulatory frameworks. Patterns from the past may not persist.

Data mining risk: Searching historical data for repeating patterns can identify coincidental relationships that do not repeat. Many apparent seasonal effects weaken or disappear when tested rigorously.

External shocks dominate: Major events such as regulatory announcements, macroeconomic shifts, or technological milestones have repeatedly overridden any calendar tendencies.

No predictive power: Even when a pattern appears in historical data, it provides no guarantee of repetition. Markets incorporate new information continuously.

In practice, seasonal narratives often receive amplified attention during periods of uncertainty or after notable price moves. This can influence short-term trader positioning and media coverage, creating temporary sentiment effects without altering underlying fundamentals.

How Beginners Users Can Use This Information

Seasonal discussions can serve as educational context for understanding how market participants interpret data and form narratives. Here is how to approach them responsibly:

Treat historical monthly averages as descriptive statistics, not forecasts.

Cross-reference multiple independent data sources rather than relying on any single chart or claim.

Combine calendar observations with other analytical frameworks, such as on-chain metrics, network fundamentals, macroeconomic indicators, and risk management principles.

Maintain consistent position sizing and risk controls regardless of seasonal commentary.

Focus on time horizons and personal financial goals rather than attempting to time entries based on month-of-year patterns.

FAQ

Is July always a positive month for Bitcoin?

No. While the average return has been positive in available data since 2013, several years recorded flat or negative July performance. Individual results vary widely.

Does the bullish July narrative mean Bitcoin will rise in July 2026 or future years?

No. Historical averages describe past outcomes only. They do not predict future price movements. Many factors beyond the calendar month influence Bitcoin’s price.

Why do some analysts highlight July specifically?

July often follows periods of relative weakness in June in certain datasets, creating a statistical contrast that draws attention. Media and commentary can amplify such observations during active market discussions.

How reliable are seasonal patterns in cryptocurrency markets?

They are generally considered low-reliability signals due to Bitcoin’s relatively short history, evolving market structure, and the dominance of fundamental and macroeconomic drivers. Patterns observed in small datasets often fail to persist.

What should someone new to crypto focus on instead of seasonal narratives?

Core concepts such as how Bitcoin’s network operates, wallet security basics, the difference between holding and trading, understanding volatility, and developing a personal research process provide more durable foundations than calendar-based observations.

Are there other months with notable historical tendencies?

Yes. Analyses frequently note stronger average performance in months such as October and November, and weaker tendencies in September in some longer datasets. All such observations share the same limitations discussed above.

Disclaimer: This content is for educational and informational purposes only and is not financial advice. Nothing here is a recommendation to buy or sell any asset or use any platform. Do your own research and manage your risk.

The Crypto Anti-Phishing Checklist: 12 Habits That Stop Wallet Drainers in 2026

How Cross-Chain Bridges Work: A Security Guide for New Crypto Traders

Cross-Chain Bridges: A Plain-English Guide to How They Work and When to Avoid Them

Need deeper training?

Join our structured modules with live examples and expert checklists for effective implementation.

JOIN THE ACADEMY